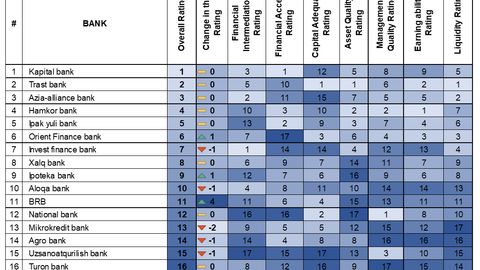

Five of Uzbekistan's leading banks drop in CERR's 2Q24 activity index rating

Moxinur Sultanova

Good news:

Grow your business with us

Advertise on Daryo.uzIndividual approach and exclusive materials

Ad-free site readingSubscribe

25 000 sum per month

Comments

To leave a comment, first