ING has initiated regular coverage of Uzbekistan. The bank’s chief economist, CIS, Dmitry Dolgin and EM sovereign strategist James Wilson, take a broad look at what the recent geopolitical shift in the CIS region as well as domestic developments mean for the country’s economic activity, fiscal and monetary policy, interest and exchange rates. They also take a snapshot of what the bank sector lending looks like.

Country view

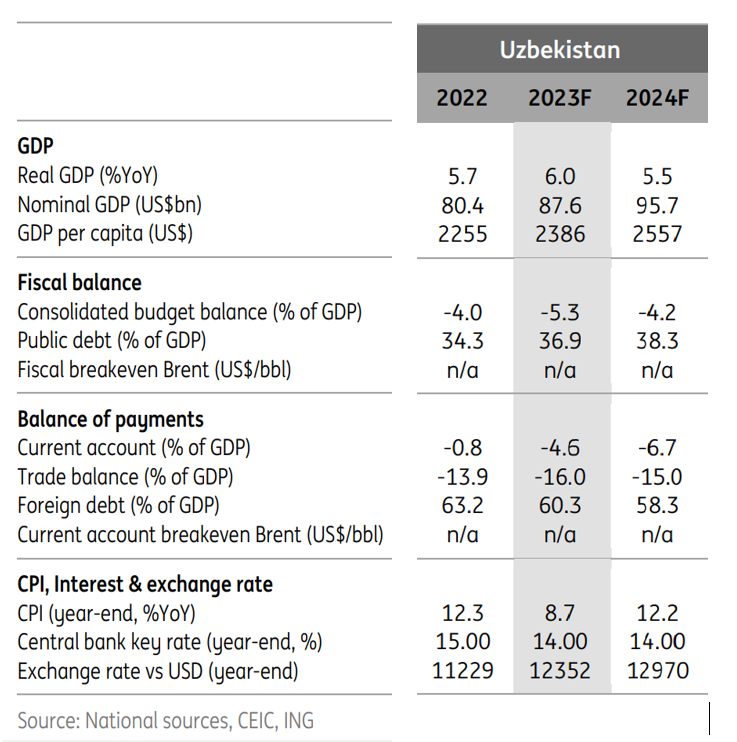

Uzbekistan is posting solid economic growth rates and is increasingly affected by fiscal policy, which is showing signs of easing in 2023. The key focus is on the soum, which has been the worst-performing currency in the CIS space. We do not exclude the possibility that the next couple of quarters could bring some temporary relief.

Economic overview

Uzbekistan is being strongly affected by fiscal policy. Its active state investments and expanding social safety net amid tax easing are supportive of economic growth and social development, but lead to a wider fiscal deficit and higher borrowing requirements.

- The monetary policy is cautious, targeting highly positive real rates to limit the monetary inflation risks coming from credit- and fiscally-sponsored demand, weaker domestic currency, and an expected inflationary effect of retail energy tariff liberalisation coming in May next year.

- The key rate currently has very little downside in 2024.

Meanwhile the Uzbekistani soum (UZS), which has been on a depreciation path for some time, may find some temporary relief in the coming couple of quarters thanks to some stabilisation in the trade and services balance, higher foreign borrowing by the government, highly positive real domestic rates, the weaker dollar on the global market, and some possible stabilisation of the currencies of Uzbekistan’s major trading partners.

Economic activity

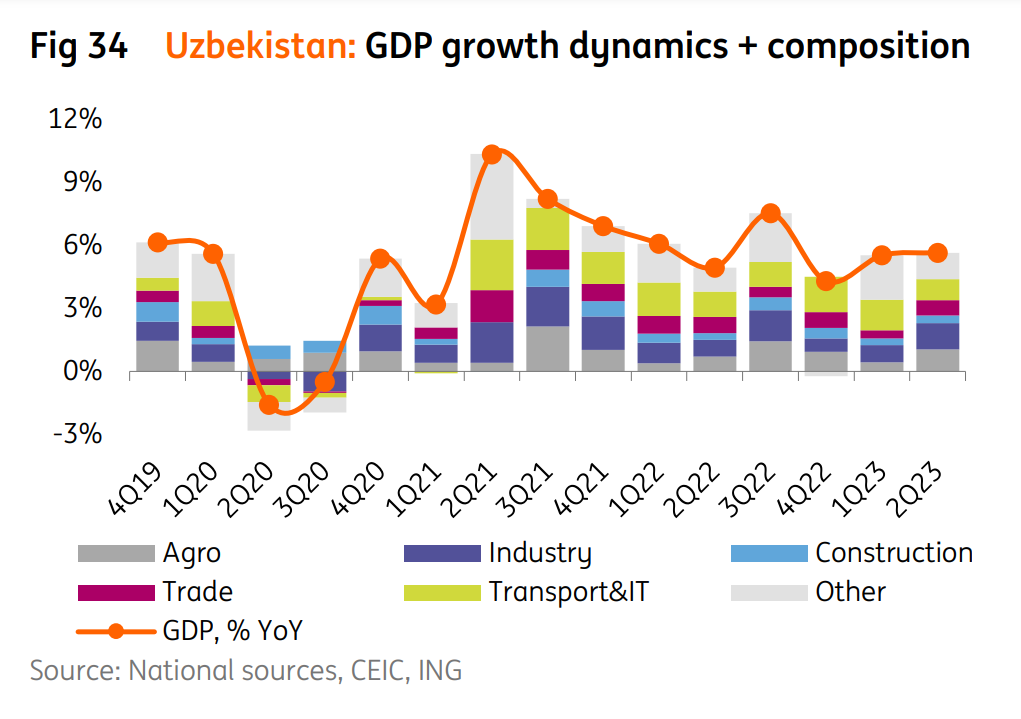

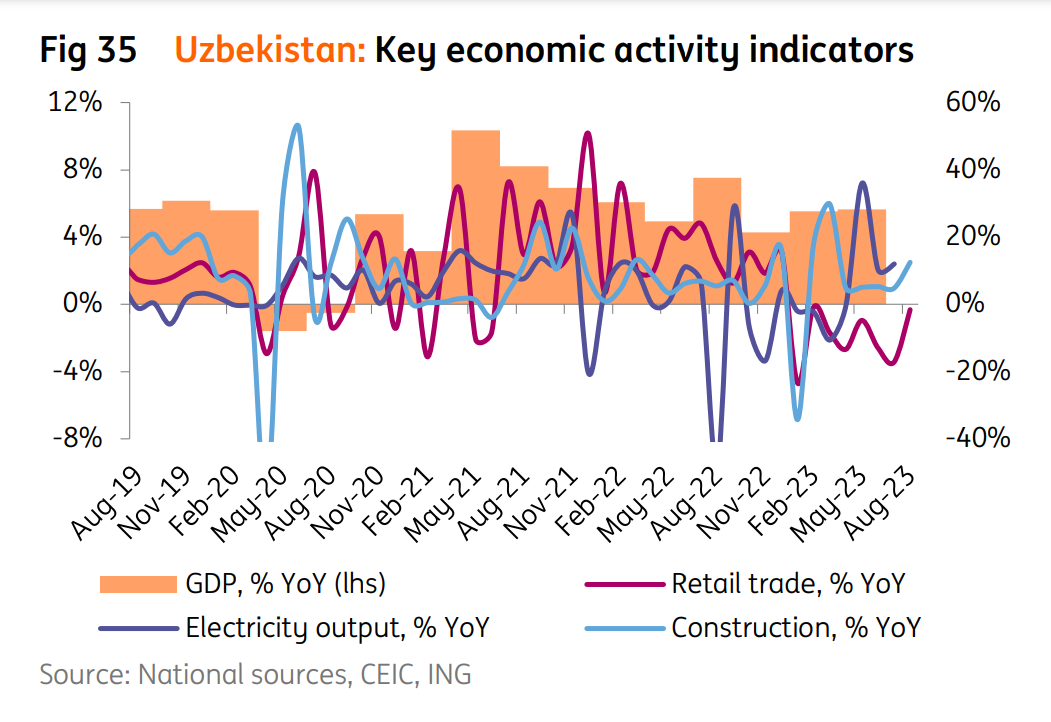

Economic activity is back on an acceleration path in Uzbekistan following a slight hiccup at the beginning of the year when activity was disrupted by power outages. GDP growth was up 5.5-5.7% YoY in 1H23, as output in agriculture and heavy industries normalised.

Domestic demand appears well supported by credit expansion, with retail lending up 40% YoY in real terms, continued remittances inflow and other spillover effects of the Russia-Ukraine conflict, continued export growth, and – most recently – by the fiscal side, as contrary to our initial expectations the consolidated budget deficit widened by almost 1ppt of GDP over the course of 1H23.

We see GDP growth picking up 0.3ppt to 6.0% in 2023 and stabilising in the normal 5.5-6.0% range in 2024-25.

Budget policy

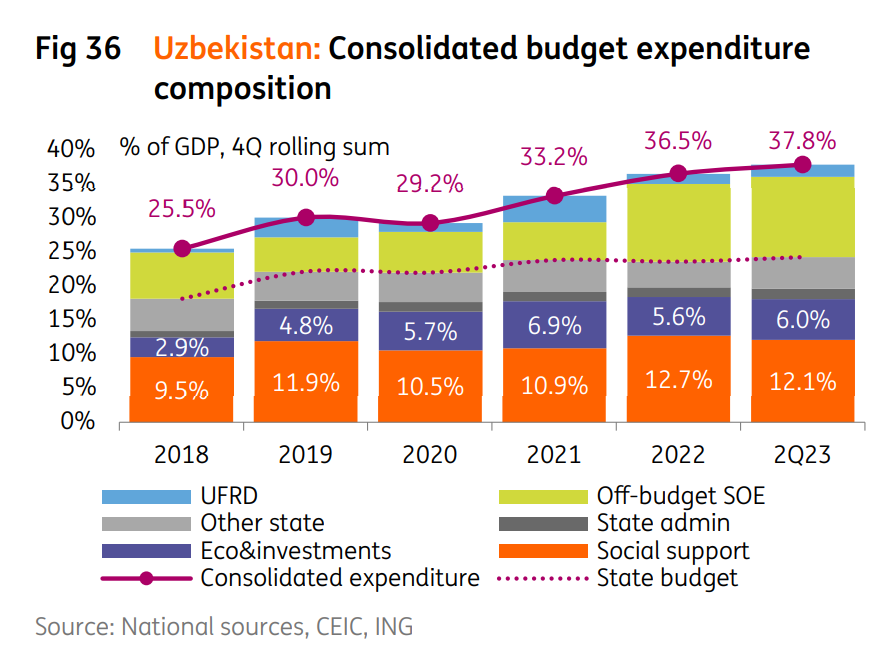

Budget policy is growth-supportive as, after consolidating from 5.5% to 4.0% of GDP in 2022, the consolidated budget deficit (comprising of state budget, sovereign fund, and budget SOEs) widened again to 4.9% of GDP on a 4Q rolling basis as of mid-2023.

- The spending increase seems to be driven by the social sphere (12-13% of GDP) including energy subsidies to low-income families and families with children, as well as state investments (6% of GDP).

- In the meantime, revenues under pressure of a reduction in VAT are negatively affected by the lower prices of Uzbekistan’s commodity exports (export-driven revenues account for around 20% of the consolidated budget). As a result, we see the consolidated budget deficit widening to 5.0-5.5% of GDP this year with some stabilisation in the 3-4% range possible within the next two years.

Public debt

With only 10% of GDP of liquid state savings in the UFRD, the sovereign fund, borrowing seems to be the primary source of the deficit. Most of Uzbekistan’s public debt is external, however, we do not exclude an attempt to boost domestic borrowing as well. The public debt, at 34% of GDP in 2022, may increase by around 5ppt by the end of 2025.

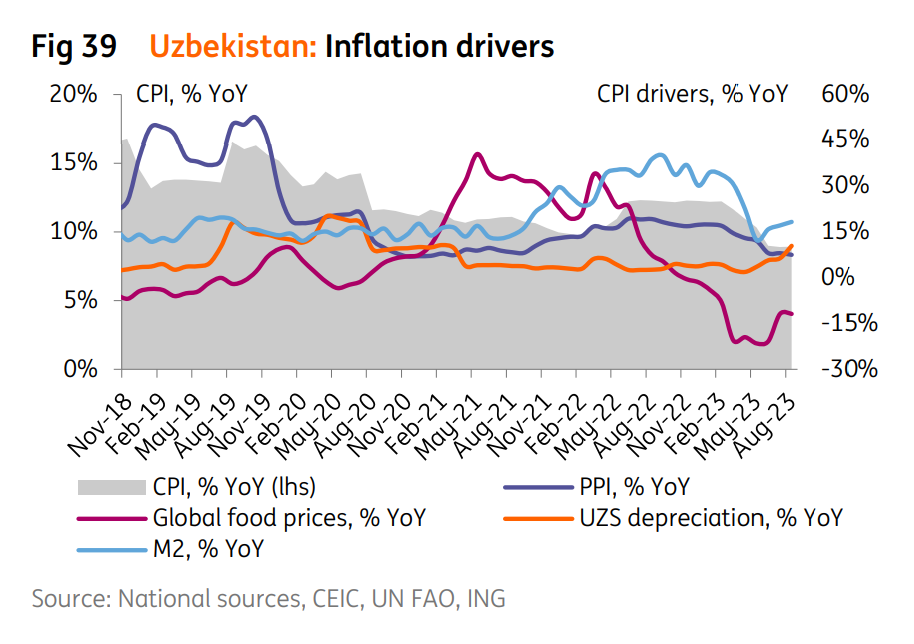

Inflation and monetary policy

Inflation appears to be on a downward path, in line with global and regional trends, with the CPI rate down to 8.9% YoY in August from the 2022 peak of 12.3%. In the meantime, the central bank is reluctant to cut the key rate of 14.0% (in place since March this year) citing elevated consumption, strong credit growth, fiscal easing, a weakening soum, and uncertainty over the impact of upcoming energy price liberalisation scheduled for next May.

CPI may stay in the 8.0-8.5% YoY territory until May 2024, after which, if the government proceeds with the spike in the tariffs, inflation may pick up again. In this environment, the NBU’s key rate of 14.0% may well have to be kept unchanged until the beginning of 2025, when the dust from the higher services inflation settles.

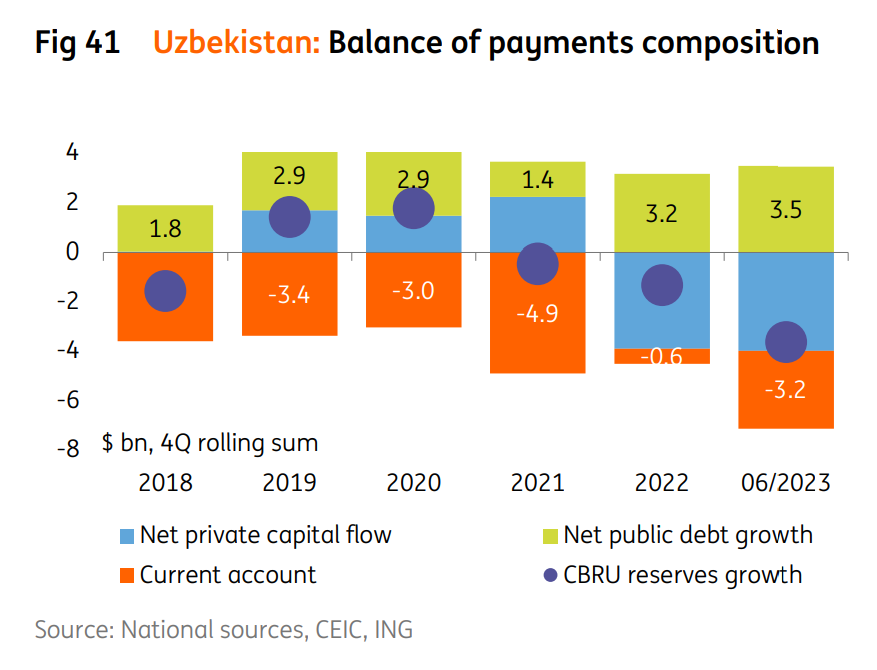

Balance of payments and exchange rate

UZS is the worst-performing currency in our covered CIS space. From a current account perspective, the balance of trade of goods and services continues to deteriorate due to elevated imports from China (probably related to the large state investment programme), but the pace of deterioration somewhat slowed.

Exports are also expanding, but not to Russia, which is positive from the perspective of secondary sanctions risk. On the remittances side, which is the main link with Russia and ruble exchange rate, the flow has moderated but remains elevated. As a result, the current account, having shown a minimal deficit of $0.6bn in 2022, has widened to a more standard $3.2bn as of mid-2023 (4Q rolling basis).

In terms of capital flows, the private sector remains a large exporter of capital ($4.0bn outflow over the past four quarters) for the second year in a row through purchases of foreign assets. Only the state sector is supporting the balance of payments, through continued attraction of foreign debt (up $3.5bn YoY) and the sale of international reserves.

While report shows that it is anticipated that Uzbekistan's currency may continue to depreciate over the long run, there's a possibility of a temporary slowdown or even a pause in this depreciation in the next few quarters. This could be influenced by factors such as increased foreign borrowing by the Uzbek government, the normalization of private capital flows following geopolitical events related to Russia, and our global outlook, which suggests the stabilization of the USD compared to Uzbekistan's key trading partners.

Uzbekistan faces both opportunities and challenges in its economic landscape. While the economy is poised for growth, fiscal policies, inflation, and currency stability remain crucial factors to monitor.

Follow Daryo's official Instagram and Twitter pages to keep current on world news.

Comments (0)